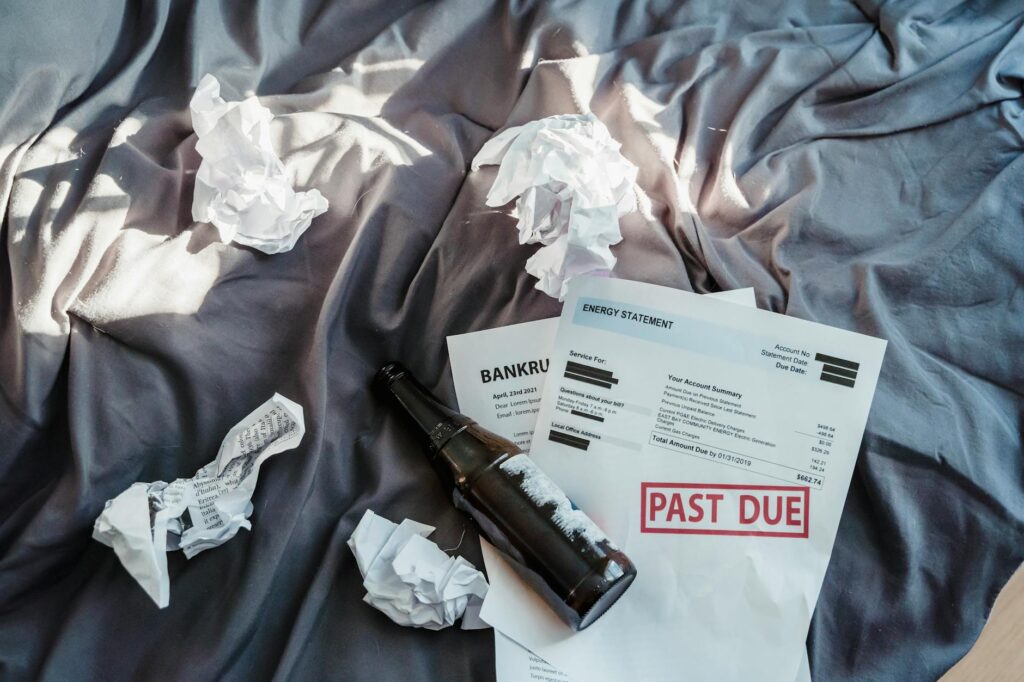

Pros and Cons of Bankruptcy & Defaults

Introduction

In the heart of every bustling city, in the quiet corners of rural towns, lives a stark divide—a chasm that separates the affluent from the financially struggling. Bankruptcy and defaults are two terms that echo through the lives of many, often cloaked in stigma yet laden with real human stories. They are not merely financial terms; they symbolize despair, hope, and the relentless pursuit of survival in a system that often seems rigged against the vulnerable. As we delve into the intricacies of bankruptcy and defaults, we explore the raw emotions and complexities that underpin these experiences, revealing how they shape lives and communities.

What Is Bankruptcy & Defaults?

At its core, bankruptcy is a legal process that provides individuals or businesses overwhelmed by debt a fresh start. It is a lifeline for some, a last resort for others. Defaults occur when borrowers fail to repay their loans, leaving creditors in a lurch. These terms encapsulate the struggle of countless individuals who find themselves ensnared by financial obligations that spiral beyond their control. Imagine a single mother, juggling two jobs to make ends meet, yet unable to pay for her child’s medical bills. The weight of such a scenario can lead her to consider bankruptcy—a decision that can feel like both a surrender and a desperate hope for a new beginning.

Why It Matters

The implications of bankruptcy and defaults ripple far beyond the individual. They touch upon societal structures, economic stability, and the very fabric of community life. For those in poverty, the stigma of bankruptcy can feel insurmountable. It’s not just about losing possessions or credit scores; it’s about losing dignity, feeling like a failure, and facing judgment from society. On the opposite end, wealthy individuals often navigate these waters with more fluidity. They may leverage bankruptcy as a strategic tool, a calculated risk that can pave the way for greater future profits. The stark contrast in experiences raises profound questions about morality, privilege, and the often invisible barriers that keep the rich insulated from the struggles of the poor.

Key Facts and Statistics

Statistically, the landscape of bankruptcy is sobering. In 2021, there were over 400,000 personal bankruptcy filings in the United States alone, a staggering number that underscores the prevalence of financial distress. Furthermore, studies reveal that minorities and low-income families are disproportionately affected by defaults and bankruptcies. This statistical reality is not just numbers on a page; they represent real lives affected by systemic issues such as inadequate access to education, healthcare, and job opportunities. The emotional toll of these facts cannot be overstated—each statistic is a reminder of a family struggling to maintain hope in an unforgiving economic climate.

Impact on Wealth and Poverty

The consequences of bankruptcy and defaults extend deeply into the fabric of wealth distribution. When individuals declare bankruptcy, they often lose not just their savings and assets, but also their ability to build wealth in the future. The emotional aftermath can be devastating. Picture a hardworking family, once thriving, now facing eviction after they default on their mortgage. The children, once secure in their home, now feel the anxiety of uncertainty. The cycle of poverty tightens its grip, making it nearly impossible for them to break free.

Conversely, the wealthier segments of society often emerge relatively unscathed, using bankruptcy to restructure debts while maintaining their lifestyle. This disparity creates a widening gap—where the rich can leverage their resources to recover, the poor are left to navigate a seemingly insurmountable wall of debt. The emotional and psychological impact of such inequality can lead to feelings of hopelessness and despair, further entrenching the divide between classes.

Real World Examples

Consider the story of Maria, a small business owner who poured her heart and soul into her bakery. After a sudden downturn in the economy, she found herself unable to pay her suppliers and her rent. The emotional turmoil was unbearable—every day felt like a new battle as she tried to salvage her dreams. Eventually, Maria was forced to declare bankruptcy. While it offered her a chance to reset, it came at a cost. She lost not just her business, but also the community she had built around it. The bakery was her identity, her joy—and losing it felt like losing a part of herself.

In contrast, think of a well-known billionaire who, after facing financial setbacks in one of his ventures, utilizes bankruptcy laws to wipe the slate clean while continuing to thrive in other investments. His losses are seen as a minor setback in a larger game of wealth accumulation. The emotional weight of their experiences differs vastly; for Maria, it was a painful end, while for the billionaire, it was merely a strategic maneuver. This stark contrast highlights the emotional and moral dilemmas surrounding wealth and poverty in our society.

Advantages and Disadvantages

Bankruptcy does offer some advantages: it can provide relief from overwhelming debt and a chance to rebuild. For many, it can feel like a new beginning, a chance to reclaim dignity after the suffocating weight of financial failure. However, the disadvantages loom large. The stigma attached to bankruptcy can result in social isolation, shame, and a lasting impact on one’s creditworthiness. For families like Maria’s, the emotional scars can take years to heal, affecting everything from mental health to familial relationships.

Defaults, while also offering a path to relief for some, can lead to long-term consequences that haunt individuals for years. The emotional toll often manifests in anxiety, depression, and a deep sense of loss—loss of dreams, aspirations, and, for many, a sense of self-worth. The journey through bankruptcy or default is often not just a financial one; it’s an emotional odyssey fraught with despair, anger, and a quest for hope.

Future Trends

As we look toward the future, the landscape of bankruptcy and defaults is likely to evolve. Economic uncertainties, changing job markets, and the ongoing impacts of global crises will influence how individuals and businesses navigate their financial challenges. The emotional ramifications of these changes will be profound. Families may find themselves in precarious situations, clinging to the hope that they can weather the storm. Meanwhile, wealthier individuals may continue to exploit loopholes, leaving the less fortunate to bear the brunt of economic instability.

The emotional landscape of bankruptcy and defaults is not just a story of numbers; it is a narrative woven with the threads of human experience. As we witness the widening gap between the rich and the poor, the stories of those struggling with debt become even more crucial.

Frequently Asked Questions

What is the emotional toll of declaring bankruptcy?

Declaring bankruptcy can lead to feelings of shame, failure, and anxiety. Individuals often grapple with the fear of judgment from society and the impact on their self-identity.

How do defaults affect mental health?

Defaults can lead to significant stress and anxiety, contributing to mental health issues like depression. The fear of losing one’s home or stability can create a persistent sense of dread.

Can bankruptcy lead to a fresh start?

While bankruptcy can offer a path to a fresh start, the emotional and social repercussions can linger long after the financial aspect is resolved.

How does wealth inequality influence bankruptcy rates?

Wealth inequality often exacerbates the challenges faced by low-income individuals in times of financial distress, making it harder for them to recover compared to wealthier individuals who can navigate the system more effectively.

What can be done to address the emotional impact of debt and bankruptcy?

Support systems, community resources, and mental health services can play a crucial role in helping individuals cope with the emotional fallout of debt and bankruptcy, fostering resilience and hope in the face of adversity.

In closing, the emotional journey surrounding bankruptcy and defaults is complex and deeply human. It reflects not just financial struggles but the very essence of our societal values and the moral imperative to address the widening gap between the rich and the poor. Each individual story matters, each experience echoes in the collective consciousness, and together they urge us to strive for a more equitable world where financial distress does not define one’s worth.